us japan tax treaty technical explanation

The tax treaty with Brazil provides a 25 tax rate for certain royalties trademark. Tax Treaty January 31 2013 Similarly the Protocol expands Japans taxation rights in respect of real property situated in Japan.

Japan United States International Income Tax Treaty Explained

Country under the provisions of a tax treaty between the United States and the foreign country and the individual does not waive the benefits of such treaty applicable to residents of the foreign.

. Income Tax Treaty PDF- 2003. Protocol PDF - 2003. Please note that treaty documents are posted on this site upon signature and prior to ratification and entry into force.

Tax Treaty is signed between the US. Article 11 provides that in cases involving a special relationship between the payor and the beneficial owner where the amount of interest paid exceeds the amount that would otherwise have been agreed upon in the absence of the special relationship then the treaty rate applies only to the last-mentioned amount that is the arms length interest payment as it is referred to. A the term Japan when used in a geographical sense means all the territory of Japan including its territorial sea in which the laws relating to Japanese tax are in force and all the area beyond its territorial sea including the seabed and subsoil thereof over which Japan has sovereign.

Japan should consider my 401k and my US private pension as retirement income for taxation purposes. How to Read and Analyze a Tax Treaty. A protocol the Protocol to the US-Japan Tax Treaty the Treaty which implements various long-awaited changes entered into force on August 30 2019 upon the exchange of instruments of ratification between the Government of Japan and the Government of the United States of America.

The Japan Protocol amends Article 231a to include a re-sourcing rule which is intended to ensure that a Japanese resident can obtain Japanese foreign tax credits for US taxes paid in cases where the United States has the primary taxing rights over an item of income. Under the amended tax treaty Japan has the right to tax capital gains on transfers of. And a foreign country in which the US.

Technical Explanation PDF - 1971. Also I tried to use this information to estimate my Japan taxes using the Japan NTA Income Tax Guide but I think I will need to consult a professional to. In the table below you can access the text of many US income tax treaties protocols notes and the accompanying Treasury Department tax treaty technical explanations as they become publicly available.

Technically a tax treaty is referred to as a Bilateral Income Tax Treaty and millions of US. Income Tax Convention the Treaty and the Canadian Department of Finance issued a press release indicating its agreement with the TE. Film royalties are taxed at 15.

The Technical Explanation is an official guide to the Convention. 1 january 1973 CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF JAPAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES. Technical explanation of the united states-japan income tax convention general effective date under article 28.

Residents on capital gains arising from the sale of shares of a company holding real property situated in Japan. US Malaysia Tax Treaty. The US and Malaysia do not currently have a tax treaty in place.

TECHNICAL EXPLANATION OF THE UNITED STATES-JAPAN INCOME TAX CONVENTION GENERAL EFFECTIVE DATE UNDER ARTICLE 28. The Protocol also amends the provisions of the existing treaty that govern the taxation of gains from the disposition of real property located in a Contacting State by a resident of the other Contracting State by defining what constitutes real property situated in the other Contracting State for purposes of Paragraph 1 of Article 13 of the existing treaty. Under the Protocol Japan is permitted to tax US.

In the table below you can access the text of many US income tax treaties protocols notes and the accompanying Treasury Department tax treaty technical explanations as they become publicly available. Is or was on good terms at the time the treaty was entered into. Department of the Treasury Technical Explanation of the most recent 2007 protocol amendments to the USCanada tax treaty.

Other Taxes in Malaysia. Convention Between the United States of America and Japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income signed at Tokyo on March 81971. Employment income is considered to be any remuneration.

It reflects the policies. The Technical Explanation is viewed by officials practitioners and scholars as an official guide to that particular convention. This is based on the US Treasury Departments technical explanation of the tax treaty.

Technical Explanation PDF - 2003. Treasury Department issues a different Technical Explanation for each tax treaty that the United States enters into. This includes wages salary bonuses or gratuity benefits-in-kind accommodationhousing allowances and compensation for loss of employment.

This article uses the current United StatesCanada income tax treaty text posted by Canadas Department of Finance. Department of the treasury technical explanation of the convention between the government of the united states of america and the government of japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and on capital gains signed at washington on november 6 2003. Taxpayers are impacted by the language found within International Tax Treaties.

Protocol Amending the Convention between the Government of the United States of America and the Government of Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income PDF. Although the TE does not amend the Protocol or the. Japan had taxing rights over capital gains on transfers of shares in a Japanese company that derives at least 50 percent of its value directly or indirectly from real property situated in Japan under the pre-amended tax treaty.

THE UNITED STATES OF AMERICA AND THE FRENCH REPUBLIC FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON ESTATES INHERITANCES AND GIFTS SIGNED AT WASHINGTON ON NOVEMBER 24 1978 Introduction This is a technical explanation of the Protocol signed at Washington on. On July 10 2008 the US. Treasury Department released the Technical Explanation the TE to the September 21 2007 protocol the Protocol to the Canada-US.

Please note that treaty documents are posted on this site upon signature and prior to ratification and entry into force. This article also refers to the authoritative US. Parent entity hereinafter Technical Explanation of Japan-US.

Japan Tax Treaty. Department of the treasury technical explanation of the protocol signed at washington on january 14 2013 amending the convention between the government of the united states of america and the government of japan for the avoidance of double taxation and the prevention of fiscal evasion with. However the WHT rate cannot exceed 2042 including the income surtax of 21 on any royalties to be received by a non-resident taxpayer of Japan under Japanese income tax law.

2

2

2

2

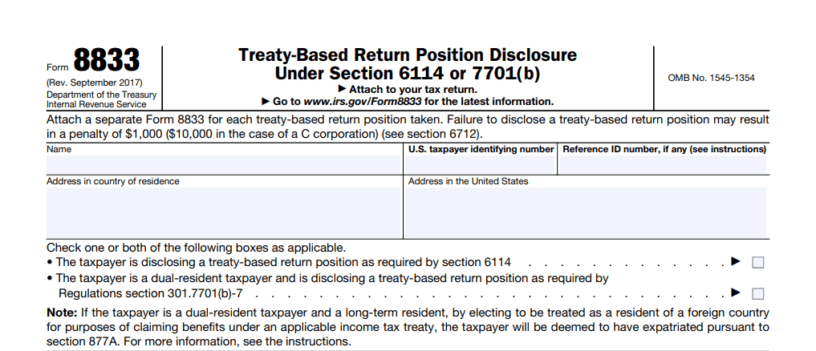

Form 8833 Tax Treaties Understanding Your Us Tax Return

Us Expat Taxes For Americans Living In Japan Bright Tax

2

2

Unraveling The United States Japan Income Tax Treaty And A Closer Look At Article 4 6 Of The Treaty Which Limits The Use Of Arbitrage Structures Sf Tax Counsel